The Inflation Puzzle

Most likely the biggest question facing global financial markets today is the outlook for inflation. Inflation helps to shape the global economy and financial markets. Globally, central banks have adopted inflation targeting as their main objective, having been haunted by previous periods of hyperinflation and deflation. They have flooded the markets with liquidity and seemed willing to risk many unknown and unintended consequences just to get inflation back to its presumed comfort zone. How should investors evaluate central banks’ behavior and how should they position their portfolios? Given the cumulative liquidity supply and additional post-Covid budgetary stimulus, should we fear hyperinflation or are authorities still just pushing on a string? This piece aims to address the inflation puzzle, in search of investment strategies that position a portfolio optimally for different inflation regimes.

Inflation confusion

Do we know what inflation is? We have defined proxies for consumer price inflation (CPI), but if you ask consumers how they experience inflation, a discrepancy often emerges. Following the onset of the COVID-19 pandemic, spending patterns changed considerably. However, the weights of items in the CPI basket take time to catch up, implying that inflation numbers partly reflect the old and not the new spending patterns.

From a macro perspective, one could argue that CPI is just one element of total inflation, so why not focus instead on the much more broadly defined GDP deflator or a global measure? For example, Switzerland has had deflation for many years, but it is still one of the most expensive countries in the world due to its strong currency. Or consider that some items have dropped out of the CPI basket because they are now available free of charge. Taking pictures and sharing them used to be expensive, but the marginal cost is now negligible. This form of hyperdeflation is invisible in our CPI statistics. Should we not distinguish between good and bad forms of inflation/deflation and address only their harmful aspects?

Money illusion

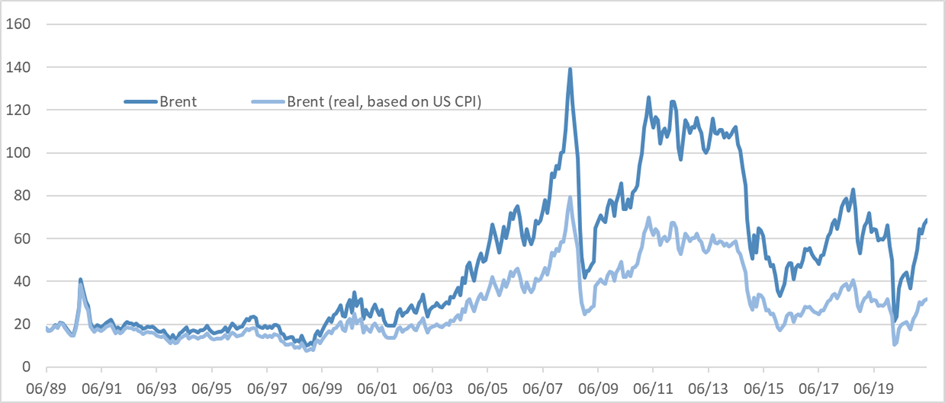

Most people suffer from the so-called ‘money illusion’, meaning that they tend to focus on nominal instead of real, inflation-adjusted prices. Steady nominal values are progressively eroded by inflation. A 7% inflation rate will halve the real value of money in about 10 years. At 2.5%, about 25% of its value is lost over a decade. As financial market professionals, we all look at nominal market indices. We chart them over long periods and compare past levels with those of today. Figure 1 shows the nominal and real prices of a barrel of Brent. Currently, the real price of Brent is only 46% of the nominal price, after adjusting for inflation since 1989.

Source: Capstone and Bloomberg

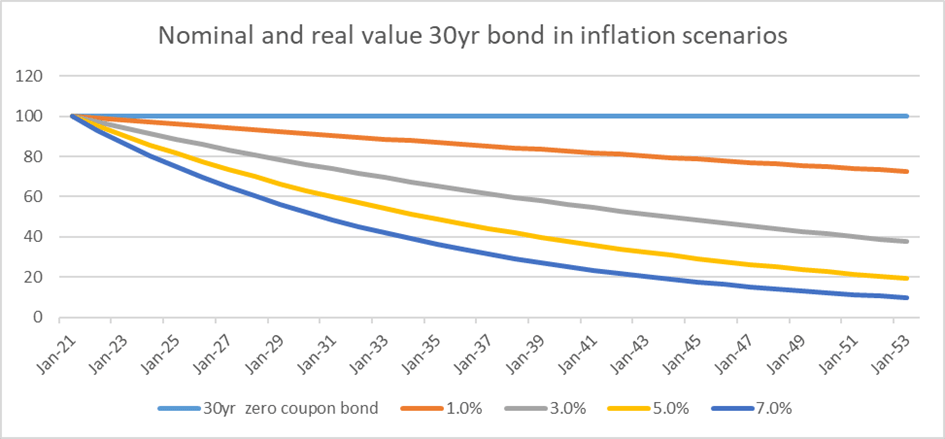

Another way of looking at the risk of inflation and the money illusion is to see what lies ahead for long-dated government bonds that were recently issued with a zero coupon. In Figure 2, one can see the devastating impact of higher inflation on the real value of these bonds at redemption.

Source: Capstone

Money illusion can also be easily exploited by governments. For instance, by freezing tax brackets, the income tax take rises every year as the real level at which higher taxes are levied decreases. There has never been a protest or demonstration in the streets against this practice.

Inflation and asset allocation

Building a portfolio that can withstand both deflationary and inflationary forces is a challenge. Most asset allocators do not seem to want to depend on getting their inflation forecast right. Predicting the inflation regime five years from now is close to impossible. On the other hand, the outcome at its extremes is either inflation or deflation and a hedge against either is directional in nature. The combination of a duration and an inflation hedge simply increases costs, as the levered positions offset each other. Obviously, this should be avoided. With that in mind we first assess some inflation protective asset classes.

Index linked bonds (ILBs) offer insurance against unexpected inflation. However, two opposing factors largely explain the returns of ILBs: inflation and duration exposure. The relationship between inflation and real yields is not always clear. In a deflationary recession, central banks steer real yields towards negative territory, leading to positive ILB returns based on duration while their inflation protection component generates negative returns. If inflation rises and central banks start to fight it, they will push real yields up. This implies a strongly negative return on ILBs due to the duration impact, which will overwhelm the inflation protection component of their return. As a result, from an absolute return perspective, as inflation protection instruments ILBs make little sense. Therefore, they should not be part of an asset mix in our view.

There are many other assets that are assumed to protect against inflation. Commodities were broadly adopted around 2000 as an asset class and an inflation hedge with a positive expected return. Back tests incorporating the 1970s showed that commodities were negatively correlated to both equities and bonds. Over that 1970s back test period, oil and other commodities rose, inflation edged up, leading to a rapid increase in bond yields and a hit to equities as profits were squeezed and economies stagnated. Also, the expected return on commodities was broken down into the spot return, backwardation (the spot price being higher than the forward price) and a cash yield, which were all assumed to be positive over the long term. However, along the way, money market rates came down to ever lower levels, backwardation was eroded by the massive entry of institutional money and spot prices started to hesitate after the supercycle of 2001-08, which was caused by the rise of China and the preceding underinvestment in manufacturing and infrastructure capacity. In addition, the correlation of commodities with bonds and equities started to change. Rising commodity prices after 2000 were mainly seen as a sign of solid world economic growth, underpinning equity markets. This led to a positive correlation between equities and commodities. After 2008, rising commodity prices were seen as a threat to global growth, increasing the risks of prolonged stagnation. Central banks, therefore, changed their reaction function and no longer responded to commodity price increases as a source of upwards pressure on inflation. Instead, they were seen as a reason to stay dovish for longer. This changed the correlation between commodities and bonds. Their low cash return, the loss of backwardation rewards and the change in correlation may have reduced the attractiveness and popularity of commodities as an asset class.

Gold is often seen as a reliable hedge against inflation, but we are skeptical. Gold has functioned as the monetary base over prolonged periods in history but we now live in a regime of fiat money. Gold has no yield, is costly to store and has a futures curve which is usually in contango (with the spot price lower than the forward price). Gold is still held by central banks, but it no longer plays an official role. It can, however, act as a protection against fear. During the deflation shock of 2007-08, gold rose considerably, but mainly due to the rapid fall in real yields as nominal yields fell faster than inflation. One reason for this is that gold is seen as an alternative to cash, especially when the (real) yield on cash and bonds is low, because this makes the relative cost of holding gold more attractive. Gold can therefore be regarded as a defensive asset class, but the link to inflation is conditional, in our opinion.

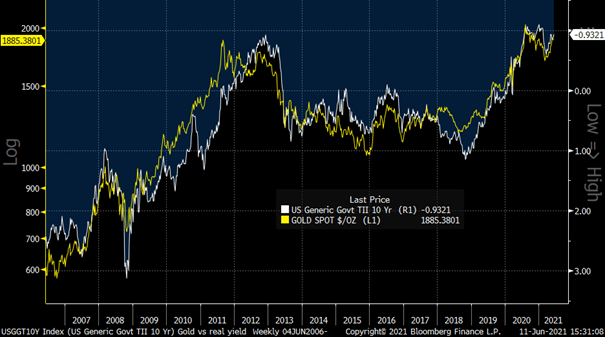

Figure 3 shows what we think is a remarkable link between gold and 10y US real yields (nominal yields minus inflation). If the link between real yields and gold holds in the future, then gold will act as an inflation hedge when inflation rises faster than nominal yields, which has not happened very often in the past decade.

Source: Capstone and Bloomberg

Another form of inflation protection can be found in assets whose cash flows are directly linked to inflation. Real estate is popular since rents are often indexed to CPI. Infrastructure such as toll roads often charge tariffs that are adjusted automatically with inflation. Again, practical experience differs significantly from theory. Real estate is highly cyclical and higher inflation and mortgage rates will typically bite into affordability, causing lower occupancy and falling real estate prices. In a recession, traffic volumes typically decline and toll road income will correspondingly reduce. A recession should be expected to increase the credit risk of corporate ILBs, which counteracts the gains made from their inflation protection component. Real estate and infrastructure are relatively illiquid asset classes and illiquidity is highly cyclical by nature. This usually greatly outweighs the benefit of cash flows that are linked to CPI.

A globally diversified investment portfolio will have exposure to a wide range of currencies and the decision to hedge or not will influence the sensitivity to an inflation shock. In general, a long US dollar exposure will act as a cushion to stress, but if the shock is commodity-driven, long exposure to currencies of commodity exporters can help to protect.

Investment horizon

Correlations to inflation depend crucially on the time horizon under consideration. The longer the horizon, the more likely it becomes that equities and real assets will prove good hedges against inflation as the underlying cash flows will ultimately keep pace with higher prices. The origin of the inflationary pressure will also determine which hedge is effective. Commodities are seen as a good hedge but will fail if, for example, prices are driven higher as a result of increases in VAT.

From a strategic perspective, we believe inflation and deflation only matter at the extremes – in the tails of the distribution – well below 0% or well above 5%. All variations within that range are more tactical in nature. Only outside this range can deflation and inflation become embedded and spiral out of control, eroding investor confidence. Following a deflationary bust, most people will want to protect themselves against deflation and few will buy inflation insurance, even though the lower the inflation rate, the higher the probability of upside surprises. Market participants tend to anchor and extrapolate. In 1982 everyone feared inflation, while until recently everyone feared deflation.

Overlay strategies

If protection against deflation is needed, one could close the duration gap between assets and liabilities, especially if a regulator imposes a nominal framework on a pension fund and liabilities are marked-to-market. Falling bond yields will then boost the present value of future liabilities and insulation we think can only be achieved through a duration overlay. In an asset-only world, running leveraged bond exposure would protect the portfolio against a deflationary bust. For this reason, risk parity strategies are among today’s survivors.

For a pension fund that marks its liabilities to market, the less obvious, but arguably much better, protection against inflation is to lower or completely remove the duration hedge. Rising inflation and yields will immediately translate into a lower present value of liabilities, thereby lifting or stabilizing the funding ratio. No other strategy will offset the impact of higher inflation more effectively than this, especially given today’s starting point, with nominal and real yields near all-time lows. For the same reason, risk parity strategies are likely to suffer, as they are geared towards a deflationary outcome.

Another powerful, but more indirect, way to manage inflation sensitivity is by adding an inflation swap overlay to the portfolio. However, as touched upon already, combining a duration and an inflation swap overlay we believe does not make sense, since the two are almost complete opposites.

Ultimately, it may be more fruitful to recognize that we do not need inflation and deflation protection all the time. Instead, we need to protect against a tail event, for instance inflation below 0% or above 5%. It is only then that profits are squeezed and central banks will pursue a more aggressive approach. Why protect yourself against inflation and pay insurance premiums in all circumstances? Currently we are in an environment where global policymakers are attempting aggressively to bring inflation back to life. If they succeed, one could argue that an increase in inflation towards approximately 4% should be welcomed by asset allocators. This is reflation – banishing the spectre of deflation – and it would be positive for most asset classes including equities, real estate and many other alternative assets. It would also help central banks to normalize monetary policy. A bear market in safe-haven bonds would be very likely, but after the repricing, bonds could offer much better value. This highlights a key take-away: safe haven bonds at today’s valuations are the most vulnerable asset class when inflation returns.

There are several ways to protect against inflationary tail risks. An investor will only fear inflation when it harms returns and need only buy protection for bear markets. This protection can be tailored to linear or convex shocks and can be implemented through options or via dynamic timing of linear instruments. If investors wish to use the full breadth of the cross-asset universe, a tailor-made trend model can potentially offer a reliable offset when inflation becomes the dominant theme.

Summary and Conclusions

Inflation drives bond as well as equity returns and through Purchasing Power Parity, currencies are anchored by it. At its extremes, inflation or deflation can start to dominate both the economy and markets. Fear of these extremes has prompted asset allocators to pay close attention to the risks. Mostly, they have discovered that there are few ways to manage them.

In general, we think the impact of inflation on a long-term portfolio is not to be feared; only in the tails does it really start to matter. Equities and most other related asset classes are effectively short a strangle on inflation (0%, 5%). As long as inflation stays within these bounds, one is likely to earn the equity risk premium. As inflation starts to escape them, it becomes important to cover the short “inflation-volatility” exposure. This calls for a dynamic approach to inflation and deflation protection. The inflation puzzle is made of many pieces and exploring this puzzle from different perspectives is the most effective approach to identifying workable solutions.

Disclaimer

Confidential & Proprietary: The content of this document is confidential and proprietary and may not be reproduced or distributed, in whole or in part, without the express written permission of Capstone Investment Advisors, LLC (“Capstone”). The content herein is based upon information we deem reliable but there is no guarantee as to its reliability, which may alter some or all of the conclusions contained herein. No representation or warranty is made concerning the accuracy of any data compiled herein. In addition, there can be no guarantee that any projection, forecast or opinion in these materials will be realized. These materials are provided for informational purposes only, and under no circumstances may any information contained herein be construed as investment advice. This document is not an offer or solicitation for the purchase or sale of any financial instrument, product or services sponsored or provided by Capstone. This document is not an advertisement and is not intended for public use or additional further distribution. By accepting receipt of this document the recipient will be deemed to represent that they possess, either individually or through their advisors, sufficient investment expertise to understand the risks involved in any purchase or sale of any financial instruments discussed herein. Neither this document nor any of its contents may be used for any purpose without the consent of Capstone.

The market commentary contained herein represents the subjective views of certain Capstone personnel and does not necessarily reflect the collective view of Capstone, or the investment strategy of any particular Capstone fund or account. Such views may be subject to change without notice. You should not rely on the information discussed herein in making any investment decision. Not investment research. The market data highlighted or discussed in this document has been selected to illustrate Capstone’s investment approach and/or market outlook and is not intended to represent fund performance or be an indicator for how funds have performed or may perform in the future. Each illustration discussed in this document has been selected solely for this purpose and has not been selected on the basis of performance or any performance-related criteria. This document is not an offer to sell or the solicitation of any offer to buy securities. Capstone is not recommending any trade and cannot since it is not a broker-dealer. Nothing in this document shall constitute a recommendation or endorsement to buy or sell any security or other financial instrument referenced in this document.

Due to rapidly changing market conditions and the complexity of investment decisions, supplemental information and other sources may be required to make informed investment decisions based on your individual investment objectives and suitability specifications. All expressions of opinions are subject to change without notice.